The Walt Disney Company reported quarterly earnings that beat expectations on Tuesday, but revenue missed estimates.

Here’s how the company did compared with what Wall Street expected:

- Adjusted EPS: $1.89 vs. $1.61 expected according to Thomson Reuters

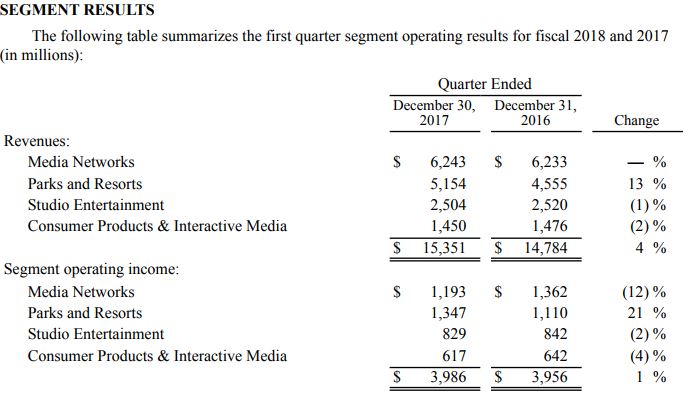

- Revenue: $15.35 billion vs. $15.45 billion expected according to Thomson Reuters

That adjusted earnings per share figure accounts for the recent tax overhaul and other one-time benefits totaling about $1.6 billion.

Shares of Disney rose about 2 percent in after-hours trade.

Disney Chairman and CEO Bob Iger told CNBC’s “Closing Bell” that the company will price ESPN Plus, the company’s first direct-to-consumer streaming service, at $4.99 per month. That product will roll out with the relaunch of the ESPN app this spring, Iger said.

Iger said ESPN Plus will offer “an array of live programming that is not available — live sports, live sports events — that is not available on current channels, and that’s by the thousands.” In a December call with analysts, Iger explained that this ESPN streaming service was really intended to be an add-on for the “ultimate sports fan” subscriber.

The ESPN announcement comes amid a 1 percent year-over-year decline in segment operating income for Disney’s cable networks business. The company said in its Tuesday release that ESPN saw lower advertising revenue in the fiscal first quarter.

A shift in the timing of the College Football Playoff games negatively impacted average viewership, the company said. These decreases at ESPN, however, were partially offset by growth at Disney Channel and Freeform.

Parks and resorts were a bright spot during the first quarter. The segment brought in $5.15 billion in revenue, besting a StreetAccount consensus estimate of $4.86 billion.

But Disney’s other businesses reported revenue that fell short of Wall Street projections. Here’s how much each segment brought in compared with what analysts projected, according to StreetAccount consensus estimates:

- Media and networks: $6.24 billion vs. $6.35 billion expected

- Parks and resorts: $5.15 billion vs. $4.86 billion expected

- Studio: $2.50 billion vs. $2.75 billion expected

- Consumer and interactive: $1.45 billion vs. $1.52 billion

Disney’s earnings report comes as its blockbuster deal with Twenty-First Century Fox looms over the rest of the entertainment industry. In December, Disney announced a $66.1 billion deal, including debt, to acquire many parts of Fox. The boards of both companies asked longtime CEO Bob Iger to stay on through the end of 2021. Fox CEO James Murdoch will help with the transition.

Still, the proposed acquisition of Fox properties will have to pass federal anti-trust laws. Investors will likely keep an eye on developments out of the Department of Justice’s lawsuit against the proposed AT&T-Time Warner merger. AT&T is slated to make its case for the deal on March 19.

The Disney-Fox deal comes as tech giants like Netflix and Amazon engage traditional medias in an increasingly competitive spending race on content. CNBC reported Monday that fear of being outspent was one of the main reasons Rupert Murdoch decided to sell those Fox assets. Last month, Netflix said it plans on spending about $7.5 billion to $8 billion on content in 2018.

Exclusive and original content help media companies market their direct-to-consumer offerings. Disney’s proposed acquisition of Fox assets would broaden the company’s content portfolio, making it more competitive.

When Disney announced that it plans on launching a stand-alone streaming service in 2019, the company said it would also be pulling its movies from Netflix. In November, Disney said it plans to price its service “substantially below” that of Netflix, in part because it would initially have a smaller library than what the streaming giant offers.

Fox is slated to report earnings after the market close on Wednesday.

This is breaking news. Please check back for updates.